What Is Low Income for a Family of 5 in the Pacific Nw

The economic downturn caused by the coronavirus pandemic has renewed attending on health insurance coverage as millions accept lost their jobs and potentially their wellness coverage. The Affordable Care Deed (ACA) sought to address the gaps in our health care arrangement that leave millions of people without health insurance past extending Medicaid coverage to many low-income individuals and providing subsidies for Marketplace coverage for individuals below 400% of poverty. Following the ACA, the number of uninsured nonelderly Americans declined by twenty 1000000, dropping to an celebrated depression in 2016. All the same, showtime in 2017, the number of uninsured nonelderly Americans increased for 3 straight years, growing by 2.2 one thousand thousand from 26.7 million in 2016 to 28.9 1000000 in 2019, and the uninsured rate increased from 10.0% in 2016 to 10.ix% in 2019.

The future of the ACA is in one case again earlier the Supreme Court in California vs. Texas, a case supported by the Trump assistants that seeks to overturn the ACA in its entirety. A decision past the Courtroom to invalidate the ACA would eliminate the coverage pathways created by the ACA, leading to significant coverage losses.

Although the number of uninsured has probable increased further in 2020, the information from 2019 provide an of import baseline for understanding changes in health coverage leading up to the pandemic. This issue brief describes trends in health coverage prior to the pandemic, examines the characteristics of the uninsured population in 2019, and summarizes the admission and financial implications of not having coverage.

| Summary: Key Facts well-nigh the Uninsured Population |

| How many people are uninsured? For the third yr in a row, the number of uninsured increased in 2019. In 2019, 28.9 million nonelderly individuals were uninsured, an increment of more than one million from 2018. Coverage losses were driven by declines in Medicaid and non-group coverage and were particularly large amongst Hispanic people and for children. Despite these recent increases, the uninsured charge per unit in 2019 was substantially lower than it was in 2010, when the first ACA provisions went into consequence and prior to the full implementation of Medicaid expansion and the establishment of Health Insurance Marketplaces. – Who are the uninsured? – Why are people uninsured? – How does not having coverage affect wellness care admission? – What are the financial implications of being uninsured? |

How many people are uninsured?

After several years of coverage gains following the implementation of the ACA, the uninsured rate increased from 2017 to 2019 amidst efforts to alter the availability and affordability of coverage. Coverage losses in 2019 were driven past declines in Medicaid and non-group coverage and were larger among nonelderly Hispanic and Native Hawaiians and Other Pacific Islander people. The number of uninsured children likewise grew significantly.

In spite of the recent increases, the number of uninsured individuals remains well below levels prior to enactment of the ACA. The number of uninsured nonelderly individuals dropped from more than than 46.v one thousand thousand in 2010 to fewer than 26.vii million in 2016 before climbing to 28.9 million individuals in 2019. We focus on coverage among nonelderly people since Medicare offers near universal coverage for the elderly, with simply 407,000, or less than 1%, of people over age 65 uninsured.

Primal Details:

- The uninsured rate increased in 2019, continuing a steady up climb that began in 2017. The uninsured charge per unit in 2019 ticked up to 10.9% from 10.4% in 2018 and 10.0% in 2016, and the number of people who were uninsured in 2019 grew past more than than 1 million from 2018 and past 2.ii meg from 2016 (Figure one). Despite these increases, the uninsured charge per unit in 2019 remained significantly below pre-ACA levels.

Figure 1: Number of Uninsured and Uninsured Charge per unit amidst the Nonelderly Population, 2008-2019

- Following enactment of the ACA in 2010, when coverage for young adults below historic period 26 and early Medicaid expansion went into effect, the number of uninsured people and the uninsured rate began to drib. When the major ACA coverage provisions went into effect in 2014, the number of uninsured and uninsured rate dropped dramatically and connected to fall through 2016 when just nether 27 1000000 people (10.0% of the nonelderly population) lacked coverage (Figure 1).

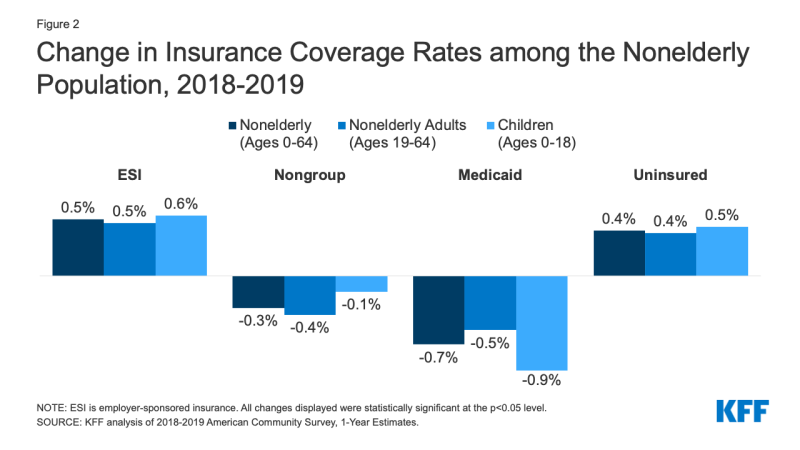

- In 2019, increases in employer-sponsored insurance were offset by declines in Medicaid and non-grouping coverage resulting in an increase in the number of nonelderly people without insurance. While the number of people covered with employer-sponsored insurance increased by 929,000, or 0.5 per centum points, from 2018 to 2019, the number of nonelderly Medicaid enrollees declined past more twice that number or 1.9 million people (0.7 per centum points). The driblet in Medicaid coverage was larger for children (0.nine percent points) compared to nonelderly adults (0.5 percent points). In add-on, the number of nonelderly people covered in the not-group market also dropped, past 879,000 from 2018 to 2019 (Figure 2).

Figure 2: Change in Insurance Coverage Rates amongst the Nonelderly Population, 2018-2019

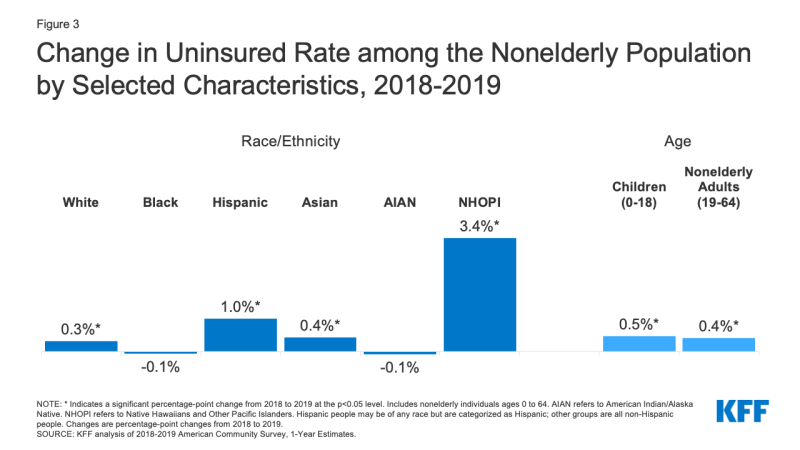

- Hispanic people and Native Hawaiians and Other Pacific Islander people experienced the largest increases in the uninsured in 2019. The uninsured rate grew i percent betoken, from xix.0% in 2018 to 20.0% in 2019 for Hispanic people and 3.4 per centum points, from 9.3% in 2018 to 12.7% in 2019 for Native Hawaiians and Pacific Islander people (Figure 3). While uninsured rates also increased for White and Asian people, the uninsured rates for Black and American Indian/Alaska Native people saw no significant alter.

Figure iii: Modify in Uninsured Rate amid the Nonelderly Population past Selected Characteristics, 2018-2019

- Hispanic people accounted for over half (57%) of the increase in nonelderly uninsured individuals in 2019, representing over 612,000 individuals. Among these uninsured nonelderly Hispanic individuals, more than than a tertiary (35%) were children.

- The number of uninsured children grew by over 327,000 from 2018 to 2019 and the uninsured rate for children ticked up nearly 0.5 percentage points from merely under 5.1% in 2018 to 5.half dozen% in 2019 (Effigy iii). While the uninsured charge per unit increased for children of all races and ethnicities, the increase was largest for Hispanic children, growing from eight.one% in 2018 to 9.ii% in 2019.

- Changes in the number of uninsured individuals varied across states in 2019. A total of xiii states experienced increases in the number of nonelderly uninsured individuals, including 9 Medicaid expansion states and four non-expansion states. Nevertheless, the uninsured rate for the group of expansion states was near half that of not-expansion states (eight.3% vs. 15.5%). Two states, California and Texas, deemed for 45% of the increase in the number of uninsured individuals from 2018 to 2019. Virginia was the only state to experience a statistically significant decrease in the number of uninsured in 2019; the state expanded its Medicaid programme that year (Appendix Tabular array A).

Who are the uninsured?

Well-nigh people who are uninsured are nonelderly adults and in working families. Families with low incomes are more probable to be uninsured. In full general, people of colour are more probable to exist uninsured than White people. Reflecting geographic variation in income and the availability of public coverage, people who live in the South or Westward are more than likely to be uninsured. Well-nigh who are uninsured have been without coverage for long periods of fourth dimension. (See Appendix Table B for detailed data on characteristics of the uninsured population.)

Cardinal Details:

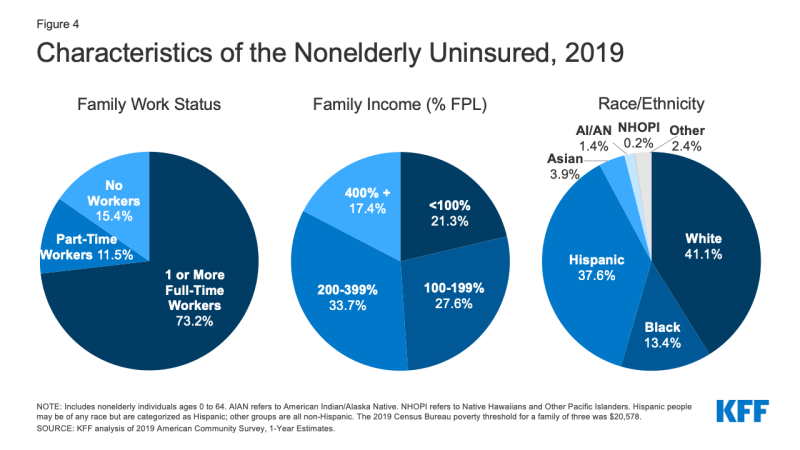

- In 2019, over seven in x of the uninsured (73.2%) had at least one full-time worker in their family and an boosted xi.5% had a office-time worker in their family (Figure four).

Effigy 4: Characteristics of the Nonelderly Uninsured, 2019

- Individuals with income below 200% of the Federal Poverty Level (FPL)1 are at the highest take chances of being uninsured (Appendix Tabular array B). In total, more than than eight in ten (82.six%) of uninsured people were in families with incomes below 400% of poverty in 2019 (Figure 4).

- Most (85.four%) of the uninsured are nonelderly adults. The uninsured charge per unit amid children was 5.6% in 2019, less than half the charge per unit amongst nonelderly adults (12.9%), largely due to broader availability of Medicaid and CHIP coverage for children than for adults (Figure 5).

Effigy five: Uninsured Rates amidst the Nonelderly Population by Selected Characteristics, 2019

- While a plurality (41.1%) of the uninsured are non-Hispanic White people, in general, people of color are at higher risk of being uninsured than White people. People of colour brand up 43.1% of the nonelderly U.S. population but account for over one-half of the total nonelderly uninsured population (Figure 4). Hispanic, Black, American Indian/Alaska Native, and Native Hawaiians and Other Pacific Islander people all have significantly higher uninsured rates than White people (7.8%) (Figure 5). However, like in previous years, Asian people have the lowest uninsured rate at 7.2%.

- Almost of the uninsured (77.0%) are U.S. citizens and 23.0% are not-citizens. Even so, non-citizens are more likely than citizens to exist uninsured. The uninsured rate for contempo immigrants, those who have been in the U.Southward. for less than v years, was 29.6% in 2019, while the uninsured charge per unit for immigrants who have lived in the US for more than v years was 36.3% (Appendix Table B).

- Uninsured rates vary by state and by region; individuals living in non-expansion states are more than probable to be uninsured (Figure 5). Fifteen of the twenty states with the highest uninsured rates in 2019 were non-expansion states as of that year (Figure 6 and Appendix Table A). Economic weather condition, availability of employer-sponsored coverage, and demographics are other factors contributing to variation in uninsured rates across states.

- Nearly seven in ten (69.five%) of the nonelderly adults uninsured in 2019 have been without coverage for more than than a year.2 People who accept been without coverage for long periods may be particularly hard to reach in outreach and enrollment efforts.

Why are people uninsured?

Most of the nonelderly in the U.Due south. obtain wellness insurance through an employer, just not all workers are offered employer-sponsored coverage or, if offered, can beget their share of the premiums. Medicaid covers many low-income individuals; however, Medicaid eligibility for adults remains limited in some states. Additionally, renewal and other policies that brand it harder for people to maintain Medicaid likely contributed to Medicaid enrollment declines. While financial assistance for Marketplace coverage is available for many moderate-income people, few people tin beget to purchase private coverage without financial aid. Some people who are eligible for coverage under the ACA may not know they tin get help and others may still observe the price of coverage prohibitive.

Central Details:

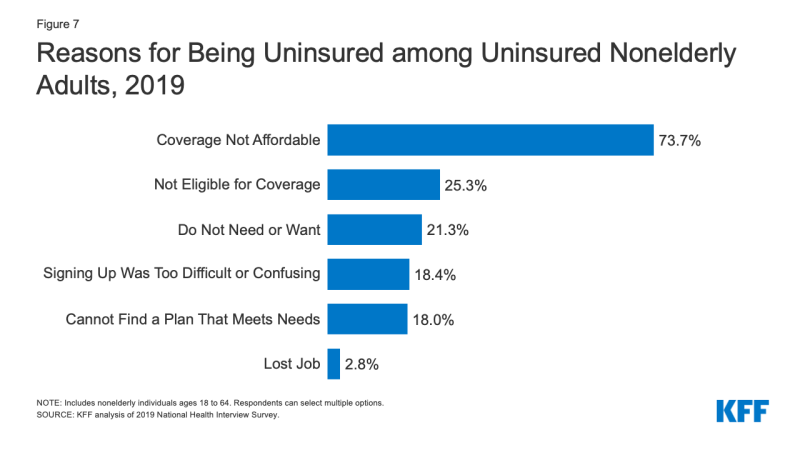

- Cost still poses a major barrier to coverage for the uninsured. In 2019, 73.7% of uninsured nonelderly adults said they were uninsured because coverage is not affordable, making it the about common reason cited for being uninsured (Figure vii).

Figure 7: Reasons for Being Uninsured among Uninsured Nonelderly Adults, 2019

- Access to wellness coverage changes as a person's state of affairs changes. In 2019, a quarter of uninsured nonelderly adults said they were uninsured because they were non eligible for coverage, while 21.3% of uninsured nonelderly adults said they were uninsured considering they did not demand or want coverage (Figure vii). Most one in v were uninsured because they constitute signing up was too difficult or confusing or they could not notice a plan to meet their needs (18.4% and 18.0%, respectively).iii Although only 2.8% of uninsured nonelderly adults reported being uninsured due to losing their job in 2019, information technology is probable the number of people who have lost their job and job-based coverage increased in 2020 due to the coronavirus pandemic.

- Equally indicated above, not all workers have admission to coverage through their job. In 2019, 72.v% of nonelderly uninsured workers worked for an employer that did not offer them health benefits.iv Among uninsured workers who are offered coverage by their employers, cost is often a barrier to taking up the offer. From 2010 to 2020, total premiums for family unit coverage increased by 55%, and the worker's share increased by xl%, outpacing wage growth.5 Depression-income families with employer-based coverage spend a significantly higher share of their income toward premiums and out-of-pocket medical expenses compared to those with income above 200% FPL.6

- Medicaid eligibility for adults varies across states and is sometimes limited. As of October 2020, 39 states including DC adopted the Medicaid expansion for adults under the ACA, although 34 states had implemented the expansion in 2019. In states that accept non expanded Medicaid, eligibility for adults remains express, with median eligibility level for parents at just 41% of poverty and adults without dependent children ineligible in most cases. Additionally, country renewal policies and periodic data matches can go far difficult for people to maintain Medicaid coverage. Millions of poor uninsured adults fall into a "coverage gap" because they earn as well much to authorize for Medicaid but not enough to qualify for Marketplace premium tax credits.

- While lawfully-nowadays immigrants under 400% of poverty are eligible for Marketplace tax credits, but those who have passed a 5-twelvemonth waiting period subsequently receiving qualified immigration status can qualify for Medicaid. Changes to public accuse policy that permit federal officials to consider use of Medicaid for non-pregnant adults when determining whether to provide certain individuals a green card are likely contributing to coverage declines among lawfully nowadays immigrants. Undocumented immigrants are ineligible for Medicaid or Market place coverage.seven

- Though financial assist is available to many of the remaining uninsured under the ACA, not everyone who is uninsured is eligible for gratuitous or subsidized coverage. Nearly half-dozen in ten of the uninsured prior to the pandemic were eligible for financial assistance either through Medicaid or through subsidized marketplace coverage. Even so, over four in 10 uninsured were outside the reach of the ACA because their state did non expand Medicaid, their income was too high to authorize for market subsidies, or their clearing condition fabricated them ineligible. Some uninsured who are eligible for help may non be aware of coverage options or may face barriers to enrollment, and even with subsidies, marketplace coverage may be unaffordable for some uninsured individuals. While outreach and enrollment help helps to facilitate both initial and ongoing enrollment in ACA coverage, these efforts face ongoing challenges due to funding cuts and high need.

How does not having coverage touch on health care access?

Health insurance makes a difference in whether and when people get necessary medical care, where they get their intendance, and ultimately, how healthy they are. Uninsured adults are far more than likely than those with insurance to postpone health care or forgo it birthday. The consequences can exist severe, particularly when preventable atmospheric condition or chronic diseases go undetected.

Cardinal Details:

- Studies repeatedly demonstrate that the uninsured are less likely than those with insurance to receive preventive care and services for major health weather condition and chronic diseases.8 , 9 , 10 , 11 More than two in five (41.5%) nonelderly uninsured adults reported not seeing a dr. or health care professional in the past 12 months. Three in ten (30.two%) nonelderly adults without coverage said that they went without needed care in the past year because of cost compared to v.three% of adults with private coverage and ix.5% of adults with public coverage. Office of the reason for poor access amongst the uninsured is that many (40.8%) practice not accept a regular place to get when they are sick or demand medical communication (Figure 8).

Figure eight: Barriers to Health Care among Nonelderly Adults by Insurance Status, 2019

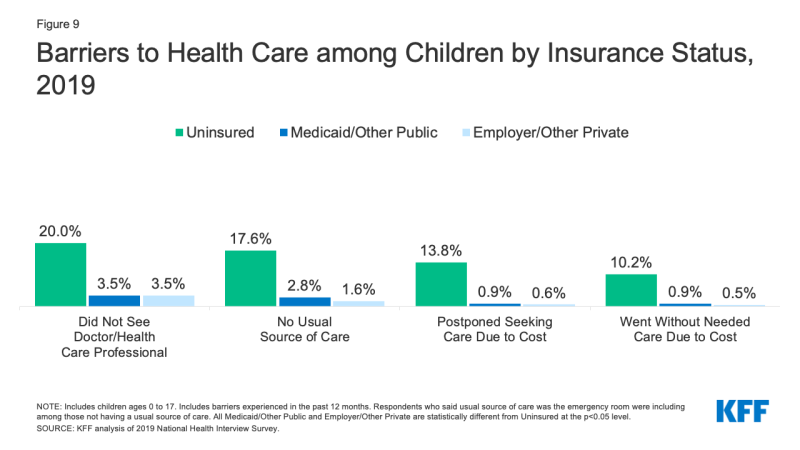

- More than 1 in ten (10.2%) uninsured children went without needed care due to cost in 2019 compared to less than one% of children with private insurance. Furthermore, one in five (20.0%) uninsured children had non seen a md in the by year compared to 3.5% for both children with public and private coverage (Effigy 9).

Figure 9: Barriers to Health Care among Children by Insurance Status, 2019

- Many uninsured people do not obtain the treatments their health care providers recommend for them considering of the cost of care. In 2019, uninsured nonelderly adults were more than iii times as likely every bit adults with private coverage to say that they delayed filling or did non get a needed prescription drug due to cost (xix.eight% vs. 6.0%).12 And while insured and uninsured people who are injured or newly diagnosed with a chronic condition receive like plans for follow-upward care, people without health coverage are less likely than those with coverage to obtain all the recommended services.13 , 14

- Considering people without wellness coverage are less likely than those with insurance to have regular outpatient intendance, they are more likely to be hospitalized for avoidable health issues and to feel declines in their overall health. When they are hospitalized, uninsured people receive fewer diagnostic and therapeutic services and likewise have higher mortality rates than those with insurance.15 , 16 , 17 , 18 , 19

- Research demonstrates that gaining health insurance improves access to health care considerably and diminishes the adverse effects of having been uninsured. A comprehensive review of enquiry on the effects of the ACA Medicaid expansion finds that expansion led to positive effects on admission to care, utilization of services, the affordability of care, and financial security among the depression-income population. Medicaid expansion is associated with increased early-stage diagnosis rates for cancer, lower rates of cardiovascular bloodshed, and increased odds of tobacco abeyance.20 , 21 , 22

- Public hospitals, community clinics and health centers, and local providers that serve underserved communities provide a crucial wellness care safety net for uninsured people. All the same, safety net providers have limited resources and service capacity, and not all uninsured people take geographic access to a safe net provider.23 , 24 , 25 High uninsured rates also contribute to rural hospital closures, leaving individuals living in rural areas at an even greater disadvantage to accessing care.

What are the financial implications of beingness uninsured?

The uninsured often face unaffordable medical bills when they do seek care. These bills can rapidly interpret into medical debt since nearly of the uninsured accept low or moderate incomes and accept little, if whatsoever, savings.26 , 27

Primal Details:

- Those without insurance for an entire calendar year pay for nearly half of their care out-of-pocket.28 In addition, hospitals oft accuse uninsured patients much college rates than those paid by private health insurers and public programs.29 , 30 , 31

- Uninsured nonelderly adults are much more likely than their insured counterparts to lack confidence in their ability to afford usual medical costs and major medical expenses or emergencies. More than 3 quarters (75.6%) of uninsured nonelderly adults say they are very or somewhat worried most paying medical bills if they become sick or have an accident, compared to 47.half-dozen% of adults with Medicaid/other public insurance and 46.i% of privately insured adults (Effigy 10).

- Medical bills can put groovy strain on the uninsured and threaten their financial well-beingness. In 2019, nonelderly uninsured adults were nearly twice as likely as those with private insurance to take problems paying medical bills (24.one% vs. 11.6%; Figure ten).32 Uninsured adults are also more likely to face negative consequences due to medical bills, such as using upward savings, having difficulty paying for necessities, borrowing coin, or having medical bills sent to collections resulting in medical debt.33

Figure 10: Bug Paying Medical Bills past Insurance Status, 2019

- Though the uninsured are typically billed for medical services they apply, when they cannot pay these bills, the costs may become bad debt or uncompensated care for providers. State, federal, and private funds defray some but not all of these costs. With the expansion of coverage under the ACA, providers are seeing reductions in uncompensated care costs, particularly in states that expanded Medicaid.

- Research suggests that gaining wellness coverage improves the affordability of care and financial security among the low-income population. Multiple studies of the ACA have found larger declines in trouble paying medical bills in expansion states relative to non-expansion states. A split up study establish that, among those residing in areas with high shares of low-income, uninsured individuals, Medicaid expansion significantly reduced the number of unpaid bills and the amount of debt sent to third-party collection agencies.

Determination

The number of people without health insurance grew for the third year in a row in 2019. Recent increases in the number of uninsured nonelderly individuals occurred amidst a growing economy and before the economic upheaval from the coronavirus pandemic that has led to millions of people losing their jobs. In the wake of these tape task losses, many people who have lost income or their task-based coverage may authorize for expanded Medicaid and subsidized marketplace coverage established past the ACA. In fact, recent data signal enrollment in both Medicaid and the Marketplaces has increased since the commencement of the pandemic. Nonetheless, it is expected the number of people who are uninsured has increased farther in 2020.

Drops in coverage among Hispanic people drove much of the increment in the overall uninsured rate in 2019. Changes to the Federal public charge policy may be contributing to declines in Medicaid coverage amongst Hispanic adults and children, leading to the growing number without health coverage. These coverage losses also come every bit COVID-19 has hitting communities of color disproportionately hard, leading to higher shares of cases, deaths, and hospitalizations among people of color. The lack of wellness coverage presents barriers to accessing needed care and may pb to worse health outcomes for those affected past the virus.

Even as the ACA coverage options provide an important rubber internet to people losing jobs during the pandemic, a Supreme Courtroom ruling in California vs. Texas could accept major effects on the entire health intendance system. If the court invalidates the ACA, the coverage expansions that were key to the law would be eliminated and would consequence in millions of people losing health coverage. Such a large increase in the number of uninsured individuals would reverse the gains in access, utilization, and affordability of care and in addressing disparities achieved since the law was implemented. These coverage losses coming in the heart of a public wellness pandemic could further jeopardize the health of those infected with COVID-19 and exacerbate disparities for vulnerable people of color.

Source: https://www.kff.org/uninsured/issue-brief/key-facts-about-the-uninsured-population/

0 Response to "What Is Low Income for a Family of 5 in the Pacific Nw"

Post a Comment